More misery for Brits as two-year fix mortgages hit post-Credit Crunch high of 6.66% – with lenders saying desperate homeowners are switching to interest-only and longer terms… so how much will it cost YOU?

- Use the mortgage calculator to see how your bills could be hit by higher rates

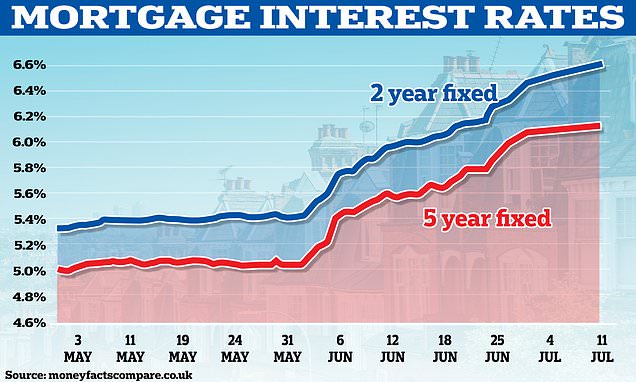

Brits are facing more misery after the average two-year mortgage fix hit a new post-Credit Crunch peak today.

The typical rate for residential loans has reached an eye-watering 6.66 per cent, according to data compiled by Moneyfacts.

That is above the grim heights during the Liz Truss meltdown last summer, and a record since August 2008.

Lenders told MPs today that customers coming off fixed rates were facing increases in costs of hundreds of pounds a month. Although the Treasury committee heard that there had yet to be a sharp increase in homeowners in distress, many were looking to increase terms or go interest-only.

Fears have been fuelled that the situation could get worse after official figures showed wages rising at a record pace, heaping pressure on the Bank of England to crack down on inflation.

However, Rishi Sunak insisted that the government must ‘stick to’ the plan to prioritise curbing prices, despite the ‘difficulties’ being cause for mortgage-payers.

Up and up: Average mortgage rates have now climbed above their previous peak after Liz Truss’s disastrous mini-Budget

The Bank of England has hikes the base rate to 5 per cent with signs that it will rise further

Fears have been fuelled that the situation could get worse after official figures showed wages rising at a record pace, heaping pressure on the Bank of England to crack down on inflation

Mr Sunak admitted inflation is ‘proving to be more persistent than people thought’ but said this does not mean his course of action is ‘wrong’

On October 20 2022, the average two-year fixed-rate mortgage hit a peak of 6.65 per cent, amid the market volatility which followed September’s mini-budget.

The average five-year fixed-rate homeowner mortgage also peaked at 6.51 per cent on that date, according to Moneyfactscompare.co.uk.

Mortgage rates later settled down, but then started to rise once more amid expectations that interest rates will be higher for longer as the Bank of England tries to subdue stubbornly high inflation.

Average two and five-year fixed-rate mortgages recently jumped back over the 6% mark.

The Bank of England uses base rate rises as a tool to try to subdue inflation and the base rate is currently sitting at 5 per cent, following 13 rises in a row.

In further signs of the pressures on inflation, new figures showed that wages have increased at a record rate.

The ONS revealed today that average regular pay, not including bonuses, was 7.3 per cent higher in the three months to May compared with the same period last year.

Moneyfacts’ figures also show that the average five-year residential mortgage on Tuesday was 6.17 per cent.

The website took the full range of mortgage deposit sizes into account.

Around 2.4million fixed-rate mortgages are due to end between now and the end of 2024, according to figures from trade association UK Finance.

Mr Sunak admitted inflation is ‘proving to be more persistent than people thought’ but said this does not mean his course of action is ‘wrong’.

Speaking to broadcasters in Vilnius, the Prime Minister acknowledged ‘things are difficult’ for families across the country amid a rise in interest rates.

‘I know things are difficult for many families across the country. The UK is not alone in experiencing a rise in interest rates… the crucial thing that we have to do is bring inflation down,’ he said.

‘That’s how we’re going to ease the burden for families. That’s how we’re going to stop the rise in interest rates. And that’s why my priority is to halve inflation.

‘Of course, that is proving to be more persistent than people thought, but that doesn’t mean the course of action is wrong. We’ve got to stick to it.’

Source: Read Full Article